The AI Opportunity: Building Trust in Wealth Management Communications

A practical framework for firms navigating agentic AI, regulatory compliance and client expectations. Why AI deployment shouldn’t erode principles of good governance

- Symphony

- Blog

Wealth Series

Part 1: Next-generation client expectations

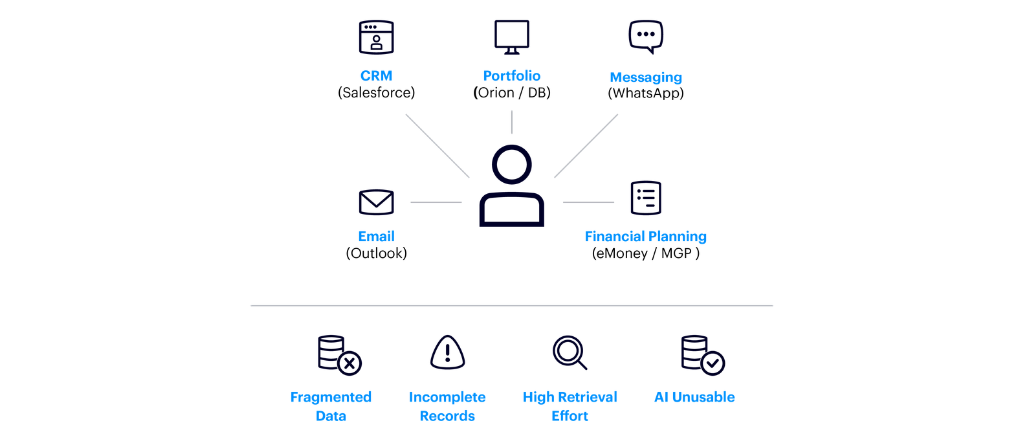

Communication workflow for wealth management

The trust paradox

Wealth management faces a real dilemma: the very technologies that promise to deepen client relationships through AI-driven personalization, mobile messaging and instant responsiveness are the same ones creating substantial compliance risk.

The SEC has levied over $2.3 billion in fines to date for off-channel communication failures, with violations appearing in WhatsApp and text messaging in 59% of recent enforcement actions against advisors. These are not edge cases or rogue actors. They represent systematic gaps between how regulated firms communicate and how clients and advisors actually prefer to communicate in practice. Meanwhile, McKinsey reports that 80% of millennial heirs, the recipients of the $84 trillion Great Wealth Transfer now underway, will seek new advisors after inheriting wealth. Mobile-first communication is cited as their main criterion for decision making. The next generation of wealth isn’t willing to email their advisor and wait 48 hours for a response.

The paradox is clear: firms that fail to modernize their client engagement model will lose assets to digital-native competitors. Yet those that rush into AI and mobile messaging without proper governance face regulatory sanctions that can damage their business and reputation. Even eroding client relationships in precisely the moments that matter most.

Wealth management leaders face a crucial challenge as AI adoption increases and firms leverage modern communication channels. Firms need to determine the optimal framework for implementation, effectively managing the transition and preserving the fiduciary trust that is fundamental to the advisor-client relationship.

Modernization in practice

The technology challenges in wealth management vary by institution size and operating model, requiring an understanding of legacy technology constraints. Understanding these distinctions is critical to mapping viable modernization strategies as firms factor in size and history.

Large global wealth managers: Integration complexity at enterprise scale

For firms managing $20 billion or more across thousands of advisors in multiple jurisdictions, the primary challenge is architectural. These institutions have invested decades and hundreds of millions of dollars building intricate, interlocking technology stacks. These include CRMs customized with proprietary workflow logic developed over the years, portfolio management systems integrated with dozens of custodians. In addition, compliance surveillance platforms that monitor email and recorded voice communications in real time. The infrastructure is sophisticated. It is also, in many places, brittle. And the seams show precisely where client expectations are shifting fastest.

The problem emerges when clients migrate to channels these systems were never meant to capture. Advisors communicate with Ultra High Net Worth (UHNW) clients via WhatsApp and iMessage, the de facto standard in relationship-driven markets across Asia, Europe, North and Latin America. In North America, iMessage and native SMS are preferred channels. These conversations occur entirely outside the CRM system’s ability to monitor for compliance. The same advisor who would never send an unarchived email about a portfolio position will text a market update from their personal phone without a second thought. This creates compliance exposure that the firm cannot measure, much less manage.

A 2024 study by Cerulli Associates found that 67% of advisors at firms with integrated tech stacks still conduct material business communications on personal devices. Notably, senior partners who manage the largest and most complex client relationships are among the most frequent violators. The compliance gap, in other words, is not technological ignorance. It is a collision between regulatory architecture built for a world of email and phone calls, and client relationships increasingly conducted in real-time mobile messaging environments. Advisors were not circumventing the rules deliberately; they were mirroring their clients.

To safely deploy agentic AI across client communications, firms must consider this as a foundational problem to address. Bringing mobile messaging channels into the same governance framework as traditional communication. Without integrated oversight across both traditional and mobile channels, AI can significantly expand risk as fragmented governance leads to greater exposure.

In practice, this shift in risk is already shaping how different segments of the wealth market approach AI adoption.

Multi-family offices and Registered Investment Advisors (RIAs): Personalization at scale

Smaller firms managing under $10 billion face a related but meaningfully distinct challenge. Unlike their larger peers, these institutions typically lack custom-built infrastructure. Instead, they deploy combinations of off-the-shelf platforms, such as Salesforce for CRM, Orion or Black Diamond for portfolio management and eMoney or MoneyGuidePro for financial planning. Each best-in-class in its category, each generating its own data model and interaction record.

The integration problem here is fragmentation. Client interactions scatter across disconnected systems: emails in Outlook, the majority of which are never logged to CRM, phone call notes residing in advisors’ memory or personal notebooks. Added to that are meeting summaries that are buried in Word documents on shared drives. Plus, WhatsApp conversations on personal devices have zero institutional visibility.

Multi-family office scenario:

For a multi-family office serving 50 UHNW families, data complexity is magnified. Imagine that each family also holds multiple legal entities across trusts, foundations, LLCs and operating companies. Add to that several custodial relationships and three generations of beneficiaries with different communication preferences and risk profiles. This fragmentation becomes untenable at scale. Before a quarterly review, the relationship manager manually searches email, checks CRM notes, reaches across the desk to a colleague and asks: “Did anyone speak with the Johnsons about their estate plan last quarter?” The institutional knowledge resides in many places. Retrieving it requires detective work. The time spent on that detective work is time not spent on advice.

These firms cannot deploy AI to personalize communication at scale when the underlying client data is incomplete and inconsistently captured. Crucially, it’s dispersed across systems that do not talk to one another. An AI assistant cannot “reach out to Sarah Johnson about her Q2 estimated tax payments” if the system has no record that her accountant flagged a potential underpayment during a call last month because that call was never logged.

The challenge for this segment is operational discipline. Establishing consistent practices for capturing client interactions, regardless of channel and linking them to the correct family entities. Thereby surfacing relevant context when advisors actually need it.

The rise of AI and agentic workflows

The rapid evolution from generative AI models that produce text, summaries and recommendations to agentic systems marks a fundamental shift in how AI operates within business workflows. Where previous AI-generated suggestions for humans to act upon, agentic systems execute actions autonomously within specific, set rules. These include monitoring and rebalancing portfolios. Or utilizing real-time data insights and sentiment scoring. They can also assist by drafting personalized client communications when market events occur. As well as bridging communication platforms and CRM systems to extract structured data to provide insights that help advisors with improved decision-making.

McKinsey estimates that 25% of enterprise AI adopters are already piloting autonomous agents, a figure expected to double by 2027. Yet the same research warns that more than 40% of agentic AI projects risk failure without strong governance frameworks and clearly defined, measurable success criteria. Gartner’s 2024 research suggested agentic AI would handle 15% of day-to-day work decisions autonomously by 2028. The technology is maturing faster than most organizations’ ability to govern it responsibly.

The wealth management use cases are genuinely compelling and worth examining concretely:

Client onboarding: Document AI agents extract structured data from identity documents, tax returns and account statements. Agents can also prepopulate Know Your Customer (KYC) and account opening forms. They also flag discrepancies for human review – compressing onboarding timelines from weeks to hours while maintaining the compliance controls that regulators require.

Portfolio monitoring: Agents continuously monitor portfolios against policy bands and generate trade recommendations when drift exceeds thresholds. They can also alert relationship managers through their preferred channel, enabling proactive rebalancing without requiring constant manual surveillance across thousands of accounts.

Communication workflows: When a client’s concentrated equity position hits a predetermined risk threshold, an agent composes a personalized message. This message explains the client’s exposure and references recent market conditions. It can then suggest specific options to diversify positions. The message is then queued for advisor review and approval before delivery via WhatsApp, email or secure messaging. This approach combines the speed of automation with the expertise of a human professional.

Compliance monitoring: Agents monitor communications across all channels, including mobile messaging platforms, flagging keywords and patterns that indicate suitability concerns or regulatory risk. It can also flag potential misconduct and route alerts to compliance staff for immediate review.

The economic logic is straightforward. As operating margins compress and competition for senior advisory talent intensifies, firms can extend genuinely personalized service to more clients without proportionally increasing headcount. But agentic systems also introduce new dependencies and failure modes that many firms are not yet equipped to manage.

The new risk surface

Model risk and fiduciary duty

An AI agent recommending a portfolio rebalance is, functionally, making an investment decision. Who bears fiduciary responsibility when an algorithm recommends liquidating a position and subsequent market conditions prove the trade was correct? And critically, who bears responsibility when they don’t?

Regulated wealth managers cannot delegate judgment to black-box algorithms because fiduciary duty is a legal and relational construct that requires identifiable human accountability. The value proposition of agentic AI depends, in part, on reducing human intervention in routine decisions. The tension is fundamental, and firms need to acknowledge it honestly rather than paper over it.

Financial Industry Regulatory Authority (FINRA) guidance on AI in June 2024 reinforced the regulatory position that firms must have “reasonably designed” supervisory systems for AI tools. In particular, addressing technology governance, model risk management and the accuracy of AI outputs. FINRA 2026 Oversight Report goes further with explicit obligations. These include requiring firms to establish robust frameworks for deploying GenAI, addressing hallucinations, bias and accuracy of model outputs.

Data governance and third-party risk

Agentic systems require comprehensive, low-latency data pipelines. Data such as CRM records, portfolio holdings, transaction history, communication logs and external market data flowing continuously into models that make real-time decisions. This creates significant surface area for data breaches, model poisoning and unauthorized data access. Consequently, leading to cascading failures when upstream data quality degrades.

Under the EU’s Digital Operational Resilience Act (DORA), which took effect in January 2025, financial institutions must maintain detailed registries of all critical third-party ICT service providers. They must conduct regular risk assessments and demonstrate contractual mechanisms for oversight and audit rights. These obligations explicitly extend to AI vendors and communication platforms, not just to core banking infrastructure. Alongside this, the Monetary Authority of Singapore (MAS) issued Guidelines on Artificial Intelligence Risk Management (AIRG) in late 2025/early 2026 to set supervisory expectations for AI in financial institutions. For wealth managers piloting agentic AI, this means treating the full technology stack as a critical operational dependency subject to the same governance discipline as core systems. Those firms that treat AI pilots as experiments are perceived as taking an informal approach to risk management that is no longer defensible.

The off-channel communication blind spot

The more acute risk is also the one often overlooked in daily operations: agentic systems can only act on data they can access. If 60 to 70% of advisor-client communication is occurring on WhatsApp and personal text messages outside institutional systems, the AI is operating on a partial picture. It is making recommendations and drafting messages. It is also generating insights based on an incomplete record of the client relationship.

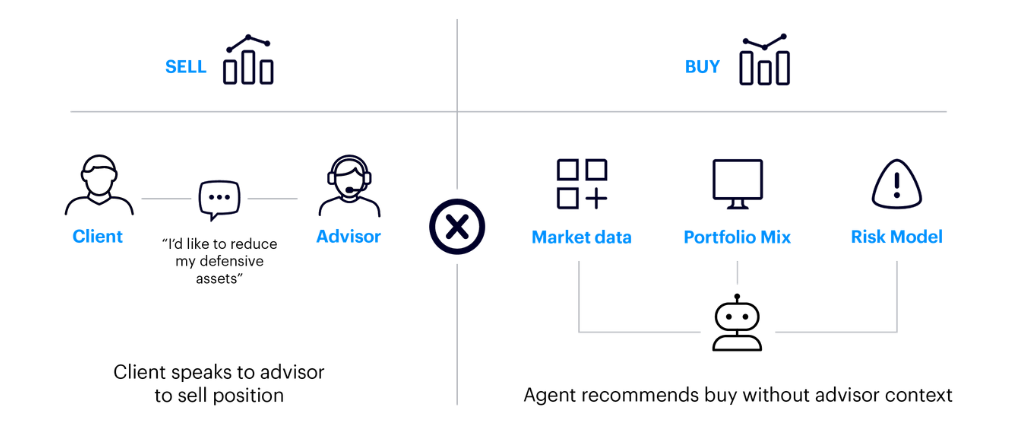

Advisor to client off-channel communication scenario:

An AI agent suggests increasing exposure to gold based on market signals, but is unaware that the client had recently told their advisor they were looking to reduce defensive positions and move into growth assets. The recommendation is logical in isolation, but out of step with the client’s stated intent. This causes the advisor to miss a better opportunity to act. The disconnect isn’t in the analysis, but in the missing context that defines the relationship.

This scenario is not hypothetical. The 2024 Investment Management Compliance Testing Survey ranked off-channel communications as the top concern for RIA compliance officers, ahead of cybersecurity and fee disclosure.

A framework for communications governance and AI deployment

The firms making sustainable progress on this are not deploying AI wholesale and hoping governance catches up. They are following a disciplined modernization sequence that treats communication governance as foundational infrastructure, ensuring compliance is embedded as a priority.

1. Close the communication governance gap. Before deploying agentic AI in any client-facing workflow, establish protocols for compliant capture and auditability for all material client communication channels. This includes email, phone, SMS and WhatsApp. As well as any other platform where advisors are actually communicating. Technology exists to solve this at scale. Compliance teams gain real-time surveillance across channels that were previously dark. Advisors gain the complete client interaction history they need to provide coherent, contextually relevant advice. Importantly, AI gains the underlying data it needs to generate recommendations that reflect the actual state of each client relationship.

The investment required is modest compared to the regulatory exposure created by off-channel violations or the competitive cost of losing next-generation clients to firms that communicate on their terms.

2. Unify data across systems. For multi-family offices and RIAs, firms that make progress treat integration as a scoped, use-case led exercise. Firms managing up to $10 billion that approach integration projects with structured methodologies, defining must-have data flows, piloting with one client segment before scaling, consistently report shorter deployment timelines, compared to those for unstructured approaches that attempt to solve everything simultaneously. The constraint is rarely technology alone: it is scope, sequencing and execution discipline.

3: Deploy AI with human guardrails. With clean data and communication governance in place, agentic systems can operate safely within defined boundaries. This aligns with current FCA Consumer Duty, DORA, FINRA, MAS AIRG and the EU AI Act by prioritizing safety, transparency and accountability. Onboarding agents pre-populate forms but require human review before submission. Portfolio monitoring agents flag rebalancing opportunities but advisors approve trades. Communication agents draft messages but queue them for advisor review before delivery. Surveillance agents detect risk indicators. Compliance staff investigate and adjudicate alerts. The model is supervised automation, balancing genuine efficiency gains with human accountability. This is important when the legal question arises about who is responsible when an algorithm recommends selling an investment.

4: Measure, learn, adjust. Treat agentic AI as a strategic initiative with defined success criteria and regular performance reviews. Track onboarding cycle time, advisor capacity utilization. Consider monitoring client engagement metrics and off-channel compliance incidents. Be prepared to course-correct when evidence suggests the technology is delivering differently than anticipated, in either direction.

A practical example of how to integrate AI agents to support communication and workflow efficiency

See a live example of AI agents for wealth & advisory workflow from our latest conference, Symphony Innovate.

Videos not loading? Check that you’ve accepted cookies or watch all on Vimeo directly here

Conclusion: Trust, amplified by technology

Traditional firms possess durable advantages that digital natives cannot quickly replicate: decades of client relationships, fiduciary credibility, access to alternative investments and the multi-generational tax and estate planning expertise that defines wealth management.

Yet these advantages erode if advisors cannot meet clients on their preferred channels. Or if governance creates operational friction that slower competitors exploit.

The execution challenge is precise: modernizing client engagement without compromising trust. Firms that close the communication governance gap, unify fragmented data and deploy AI with human oversight, unlock a competitive position distinct from both legacy incumbents and digital-first disruptors. They operate at the intersection of personalization and discipline.

The institutions that succeed will not be those deploying the most AI or the fastest. They will be those who prove that high-touch advisory and modern technology are not contradictory. They are complementary. Trust, amplified by technology, is the defining currency of next-generation wealth management.

About Symphony for Wealth Management

Symphony enables wealth management institutions to modernize client engagement through secure, connected and intelligent communications. Its platform integrates seamlessly with existing systems, allowing relationship managers to connect with clients via WhatsApp, WeChat and other preferred channels, while supporting regulatory compliance and auditability.

Symphony helps wealth management firms balance efficiency with trust. Empowering advisors to focus on relationships, not administration. The result is a model of communication fit for the age of agentic AI: secure, personalized and human-centered.